Understanding Capitalism Part V: Evolution of the American Economy

Understanding Capitalism Part V: Evolution of the American Economy

By - March 15, 2013

When the United States of America

was founded in 1787 it was the most egalitarian Western nation in the

world for citizens of European descent, indeed one of the most egalitarian major societies in all of human

history. It was the relative equality of white American society that made America

such an attractive place for European immigrants and a "land of

opportunity". Understanding capitalism, its impact on economies in

general, and its impact on America in particular, requires both a knowledge

of American economic history and an understanding of economic theory. Let's

first take a look at the history of the American economy, and then delve

into economic theory as is relates to the history of the American economy

and capitalism in general.

When America was founded noble aristocracies ruled Europe, and virtually every

major nation on earth was dominated by a feudal system of some sort or

another. In Japan, China, India, the Ottoman Empire, and across Europe,

massive under-classes of property-less peasants were dominated by a relative

few who owned and controlled the property of the nation. The Industrial

Revolution was just beginning to dawn in England, but the economies of the

world were still dominated by agriculture. As such, land was of course the

most significant form of capital and virtually all of the land in every

"civilized" nation was owned by a relative few, being split primarily among

the nobility and religious institutions.

In the British colonies of America, however, the rule of aristocracies had never been solidly

established. Though aristocrats coming to America from Europe enjoyed

initial advantages in the "New World", the widespread availability of land and

the small population meant that there was more than enough land for everyone

who came to America from Europe to obtain their own land at little or no

cost. During the early colonial period land could be obtained simply by

"right of discovery", which meant that anyone could claim any land that was

not already claimed by other Christians. This right was

granted in the colonial charters issued by the English crown, and similar

such charters were issued by other European nations for their colonies. When

land was found that was inhabited by natives, the natives were either killed,

driven off, or some trade agreement was made to ensure that the natives

would leave the land and allow the Europeans to take it over. Property

rights in the British colonies were still based on the English feudal system

however. All of the land was technically owned by the king of England, and

was considered on loan to the title holders. This made little difference in

America in terms of land use, but understanding the feudal heritage of

property right law is important for understanding the development of modern

property rights. Under the feudal system labor was not recognized as

imparting a right to property. This is because all property was owned by the

king and titles were granted to a hierarchy of administrative lords who retained

rights to the value produced using said property. Recognizing a right to

property created by labor would have unraveled the entire feudal system,

since the feudal hierarchy was effectively a hierarchy of non-laborers who

derived all of their income via ownership or title to property upon which

laborers worked and created value, which was all then owned by the title

holders - ultimately the king.

As Thomas Paine later noted in The Rights of Man:

The aristocracy are not the farmers who work the land, and raise the

produce, but are the mere consumers of the rent; and when compared with

the active world, are the drones, a seraglio of males, who neither

collect the honey nor form the hive, but exist only for lazy enjoyment. - Thomas Paine; The Rights of Man, 1791

It was in opposition to this system of ownership that John Locke famously put

forward his statements that the right to ownership of property was a product

of labor.

[E]very man has a "property" in his own "person." This nobody has any

right to but himself. The "labour" of his body and the "work" of his

hands, we may say, are properly his. Whatsoever, then, he removes out of

the state that Nature hath provided and left it in, he hath mixed his

labour with it, and joined to it something that is his own, and thereby

makes it his property. It being by him removed from the common state

Nature placed it in, it hath by this labour something annexed to it that

excludes the common right of other men. For this "labour" being the

unquestionable property of the labourer, no man but he can have a right

to what that is once joined to, at least where there is enough, and as

good left in common for others. - John Locke; Second Treaties on Civil

Government, 1690

What happened in the British colonies of America, however, was that

virtually all Europeans were able to become their own lords. While the

feudal system of property rights technically remained the same, the fact

that almost everyone (white males) owned their own capital

meant that (white male) individuals did retain ownership to the value created by their

own labor, but that right to ownership remained granted through property

rights, not through a right of labor.

Estimates from the colonial period show that land was by far the dominant

form of capital during the colonial period. It is estimated that as of 1774

land accounted for 56% of privately held wealth, with slaves accounting for

19%, livestock accounting for 9%, and tools & equipment accounting for 3%.

Ultimately land was granted in five ways within the colonies:

via ownership shares in the companies which came to America, via headright

grants (a set amount of land per person in a family), by purchase from the

local governments, by squatters rights, and via special-purpose grants from

local governments. The result of this was essentially that the most

significant capital, land, was "free" or very cheap to acquire in the New

World, which ultimately had the effect of bringing about the conditions

whereby nearly every white male was able to own their own property, and to

thus secure for themselves the right to ownership of the products of their

own labor.

Not only was land cheap and easy to acquire in the New World, but

importantly land owners had the right to do with the land whatever they

wanted, with very few limits. However taxes had to be paid on land, which

made simply holding large blocks of land and doing nothing with it generally

unaffordable. This drove a more equal distribution of land, because it was

generally only affordable to own as much land as one could actively extract

revenue from. The overall effect of this practice was to encourage

widespread family farming in colonial America, which was by design. The

colonists, and indeed even the English Crown, wanted to encourage land use,

not simply land acquisition for acquisition's sake.

Nevertheless, land speculation became quite popular in the colonies and

remained very popular well after the founding of the country. Land

speculation was the first major speculative market in America. Several

factors made land speculation an almost no-lose proposition for the early

inhabitants. Firstly, land could be acquired for next to nothing, and

secondly the population was increasing rapidly, with new people arriving

daily. Obviously this meant that people could come to America, acquire a

large amount of land at little cost, hold onto it for a short while, and

then sell it for significant profits.

All of these factors contributed to the fact that early Americans

strongly associated private capital ownership with both individual freedom

and equality. In America the right of individuals to effectively own land

and to actually be able to use it in practice, as well as to run their own

businesses largely free of the taxes and regulations imposed on businesses by the

Crown in England (which were used to benefit the aristocracy), made individuals more equal than they

were in Europe.

In Europe all property was owned by kings, and was administered via a

feudal hierarchy of nobles who collected taxes from their subjects, not

for the benefit of the public or for use in creating public goods, but

rather as their form of private income. In Europe massive inequality was a

product of consolidated property ownership, where a relatively small number

of people owned and controlled all of the property. In Europe the "property

owners" were the nobility and the church. As such, property rights in Europe

were viewed completely differently than in America. In Europe property

rights granted the nobility the right to property ownership, thereby

disenfranchising the bulk of the population. In Europe workers worked on

property owned by nobles and they had to pay a tax to the property

owners for a portion of everything that they created. These taxes were the

basis of the incomes of the nobility. The nobility generally did not

have to work at all if they didn't want to and had few obligations to use

their incomes for anything other than their personal enjoyment. Some

aristocrats gave money to charity, some didn't. Some aristocrats used their

resources to engage in scientific pursuits or to develop public works, other

used it to have orgies and elaborate parties, and of course some did all of

the above.

When Alexis de Tocqueville visited America in the early 1800s he was most

strongly stuck by the relative social and economic equality that existed in

the United States. He was so impressed by American equality in fact that it

is the first thing he mentions in his classic work

Democracy in America, and it is what he claims inspired him to

write the book. Below is the introduction to Democracy in America, published in

1835:

Amongst the novel objects that attracted my attention during my stay

in the United States, nothing struck me more forcibly than the

general equality of conditions. I readily discovered the prodigious

influence which this primary fact exercises on the whole course of

society, by giving a certain direction to public opinion, and a certain

tenor to the laws; by imparting new maxims to the governing powers, and

peculiar habits to the governed. I speedily perceived that the influence

of this fact extends far beyond the political character and the laws of

the country, and that it has no less empire over civil society than over

the Government; it creates opinions, engenders sentiments, suggests

the ordinary practices of life, and modifies whatever it does not

produce. The more I advanced in the study of American society,

the more I perceived that the equality of conditions is the fundamental

fact from which all others seem to be derived, and the central point

at which all my observations constantly terminated. I then turned my

thoughts to our own hemisphere, where I imagined that I discerned

something analogous to the spectacle which the New World presented to

me. I observed that the equality of conditions is daily progressing

towards those extreme limits which it seems to have reached in the

United States, and that the democracy which governs the American

communities appears to be rapidly rising into power in Europe. I hence

conceived the idea of the book which is now before the reader.

Tocqueville goes on to state in other sections:

As soon as land was held on any other than a feudal tenure, and

personal property began in its turn to confer influence and power, every

improvement which was introduced in commerce or manufacture was a fresh

element of the equality of conditions.

...

The social condition of the Americans is eminently democratic; this

was its character at the foundation of the Colonies, and is still more

strongly marked at the present day. I have stated in the preceding

chapter that great equality existed among the emigrants who settled on

the shores of New England. The germ of aristocracy was never planted in

that part of the Union.

...

In America there are comparatively few who are rich enough to live

without a profession. ... In America most of the rich men were formerly

poor; most of those who now enjoy leisure were absorbed in business

during their youth;...

...

America, then, exhibits in her social state a most extraordinary

phenomenon. Men are there seen on a greater equality in point of fortune

and intellect, or, in other words, more equal in their strength, than in

any other country of the world, or in any age of which history has

preserved the remembrance.

This is not to say that there was total equality in America, clearly

there wasn't, and Democracy in America has been criticized for

turning a largely blind eye to the role of slavery and other issues of

inequality in America, but what was clear was that there was much greater

equality in America among the free citizens than there was in Europe at the

time, because in America virtually everyone was a property owner. There were

still indentured servants in America, there were still people living in

poverty in the cities, women generally couldn't own property, and of course

there was slavery, but despite all these things, the level of equality was

still much much greater than in Europe, or practically any other

technologically developed society in history.

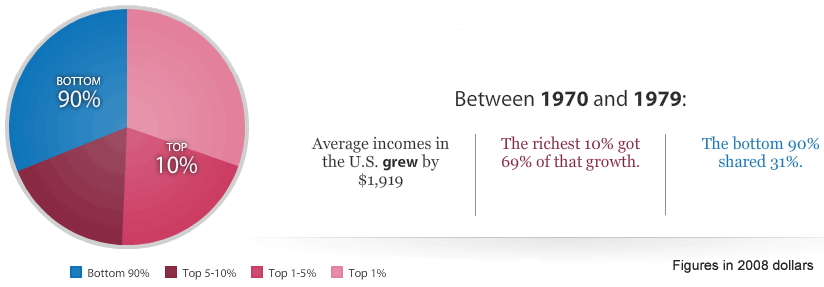

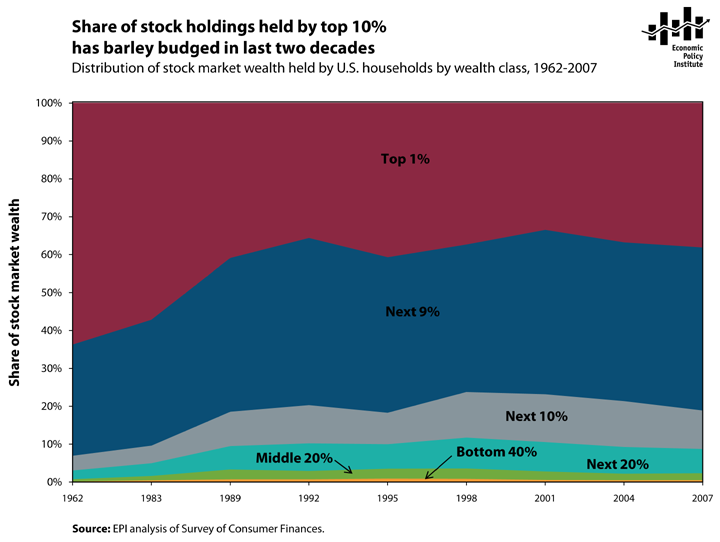

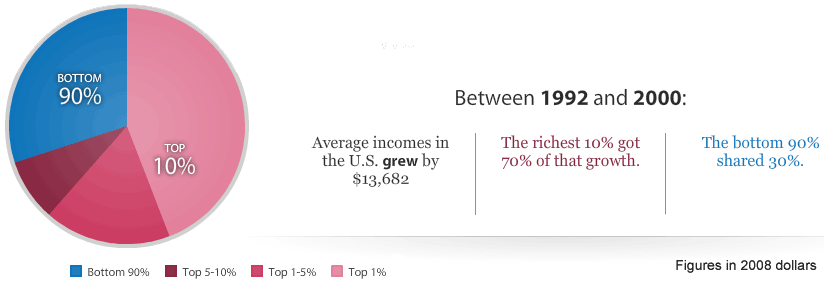

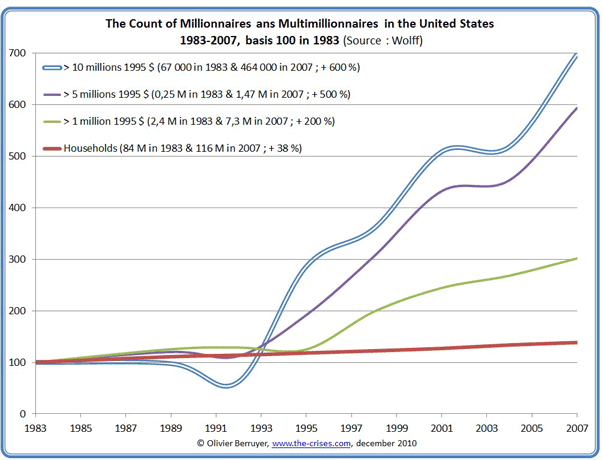

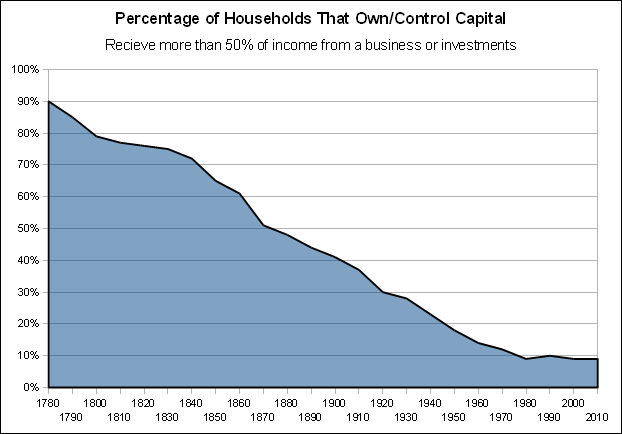

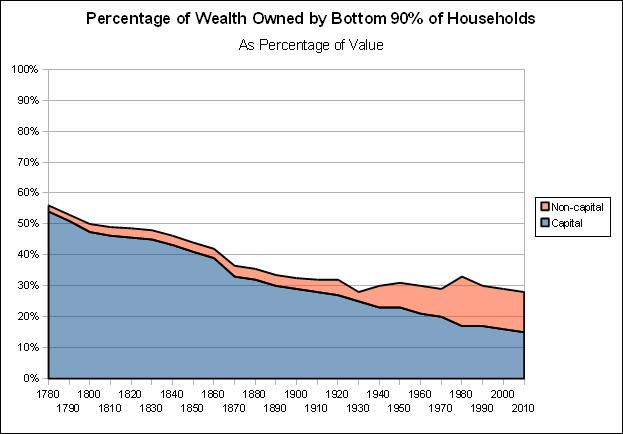

As of 1774 it is estimated that the wealthiest 10% of the population held

roughly 42% of the wealth, with the greatest disparity being in the Southern

colonies. Today, by comparison, it is estimated that the wealthiest 5% of the population

holds roughly 64% of the wealth and the top 10% holds roughly 75% of the

wealth.

At the time of the revolution roughly 85% of American colonists were

farmers, and roughly 90% of free citizens worked for themselves or in family

businesses. The remaining 10% were largely either paid free laborers

typically working in New England in places like ship yards, apprentices

working in a trade for a master craftsman, or indentured servants. Roughly

12% of the total colonial population were slaves, with about 30% of the

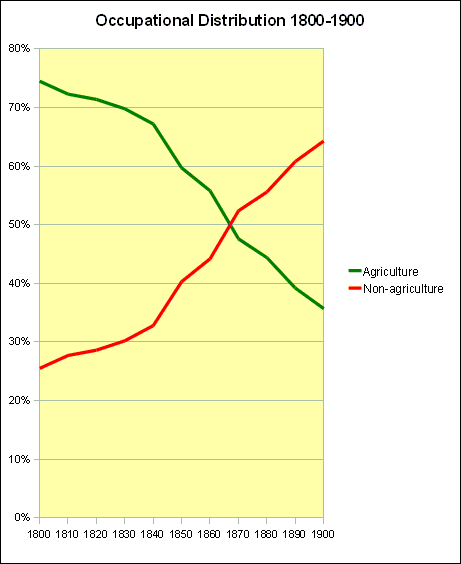

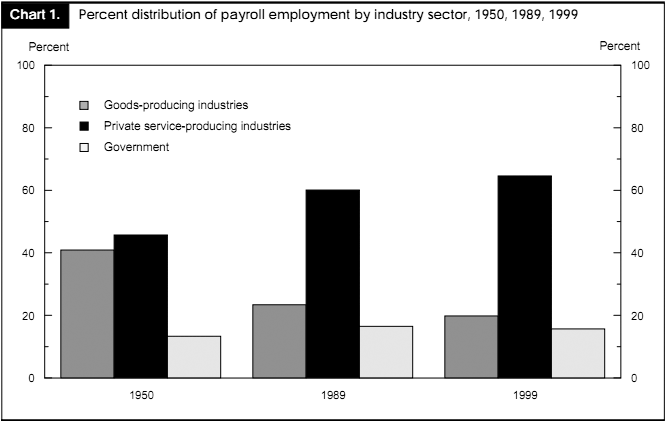

population of the Southern colonies being slaves. The graph below shows the

percentage of the American workforce dedicated to agriculture throughout the

19th century. As of 1860, just prior to the Civil War, roughly 14% of the

American workforce was working in manufacturing, with the remaining portion

of non-agricultural workers engaged in the services sector.

source: Stanley Lebergott, Manpower in Economic Growth: The American

Records Since 1800; 1963, p. 510

Due to the relationship between gender and property ownership, a large

portion of free laborers were women and children, because of course women

and children either couldn't or didn't own property. Most manufacturing

prior to the Civil War still took place in the home, but the portion of

manufacturing taking place outside the home had grown steadily over time prior to

industrialization, and became essentially the only means of manufacturing after

industrialization. In the early 19th century what happened was women and

girls who were seen as unneeded workers on family farms often left home to

travel to towns and cities where they worked as paid laborers in

increasingly mechanized collective manufacturing facilities. The dominant

manufacturing industry in early America was textile production, based

largely on the cotton supplied from the South, and it was in this industry

that many women worked. Women typically had no income at all on the family

farms (just food and boarding), so even though their incomes were low

and they were often exploited by manufactures, manufacturing gave them at

least some income and a level of independence. Male free laborers were

almost entirely first generation immigrants who had not yet obtained any

property of their own, or free non-whites. Prior to the Civil War as much as

40% of the non-agricultural workforce

was comprised of women and children, while the free agricultural workforce was only 5% female.

Female agricultural workers, other than slaves, were virtually all family

members of male farm owners. Of the women in manufacturing, essentially all

of them were unpropertied wage laborers, while most of the men in

manufacturing were both owners and workers.

women in pre-industrial home-based manufacturing

women in early industrial textile manufacturing

At this point, free laborers had very few rights. Prior to 1820 people who didn't own

property, in the form of land, home, or business, did not have the right to

vote, and free laborers had very few legal protections regarding

compensation for their labor. Workers could be fired without pay for work

done, workers could be held responsible for the cost of supplies and for

damages to capital, and if an employer went bankrupt or out of business

(which was quite common) laborers generally had no expectation of being able to receive any owed

compensation. Again, the relationship between labor and capital descended

directly from the feudal system, where all rights were defined by property

ownership because it was through property ownership that the hierarchy of

the nobility was defined. The difference in America was that every male

citizen was free to become a "feudal lord" and free laborers were free to move

from lord to lord, or to become lords themselves, but the relationship

between the propertied and the propertyless remained relatively unchanged.

While the widespread ownership of private property

was a defining characteristic of the American condition, most of the land in

America remained public property owned by states and the federal government

until after the Civil War. As of the Civil War, roughly 65% of incorporated American land

was still public domain, not privately held by anyone.

This public land was often used by individuals for private gain. The uses

of the public lands included farming, fur trapping, hunting, mining, cattle

grazing, and timber harvesting. In each of these cases, the use of public

lands essentially acted as the use of shared capital, i.e. collectively held

capital. Public lands did play an important role in providing a means for

propertyless individuals to work for themselves and generate enough wealth

to become property owners themselves. There were of course also many abuses

of the public lands, with numerous schemes where individuals created false

deeds to public lands and sold the land to individuals, in which cases

sometimes the individuals retained rights to the land and sometimes they

didn't. The public lands were also widely exploited by loggers and miners

who would in some cases clear cut the land, reaping great profits, leaving

destruction in their wake and paying no compensation to the state for their

use of the resources.

In the 1820s laws regarding the use of private property were

radically changed in America. English law had long established the right of

private property owners (remember these were mostly the aristocracy at the

time) to be free from any negative impacts on their property caused by the

use of another person's private property. This granted private property

owners prescriptive rights, meaning that their ownership granted them a right

to the quality of their property and others could not do anything that world

force unwanted externalities upon them. In practice this meant that in the

case of two land owners next to one another, the one couldn't erect a

building that would cast a shadow on the property of the other, the one

couldn't erect a mill that would muddy the waters of the other down-stream,

etc. Clearly this would stifle development, and the primary concern of early

Americans was development, so prescriptive rights were largely eliminated in

America and replaced with priority rights. Priority rights gave priority to

the property owner to modify their property and use it as they wanted, even

if it caused negative impacts on others. Under the older laws things like

pollution were fundamentally illegal, under the new laws that swept across

America pollution and negative impacts on others became the norm. The new

laws largely removed the responsibility of property owners from having to

compensate other property owners for the negative impacts that their use had

upon them. This paved the way for the development of industries that

produced noise, smoke, trash, etc., which consumed water and diverted

rivers, and which had widespread negative impacts on others in general.

By granting property owners free right to negatively impact others

through the use of their private property, this gave rise to the role of

negative externalities as a driver of profits. Negative externalities are

negative economic impacts that result from some action, the costs of which

are born by someone other than those who caused the impact. This allows

producers to produce goods more cheaply, because a portion of the cost of

production is born by others. The producer reaps the full reward for the

sale of their goods, but does not pay the full cost of production, pushing

that cost off onto others, thus increasing the profit margins of the

producer at a cost to others.

In the period from the American Revolution to the Civil War there was a

general increase in economic inequality. This was most pronounced in the

South, where slavery was practiced. Increases in inequality generally

corresponded with the decline of family farming, growing concentrations of

capital ownership (mostly in the form of land and slaves), and in the early

rise of small factories. In the South the plantation system was resulting in

growing concentrations of capital, whereby

large-scale plantations were increasing in size and in their share of the

economy. This was pushing small farmers out and leading to a growing number

of free white laborers working on large plantations instead of owning their

own farms. Likewise, the large plantations were largely self-sufficient and

independent, housing their own machine shops and producing much of their own

food and equipment, thus the growth of the plantations did not lead to

overall economic expansion in the South the way that growing factories in

the North lead to overall economic expansion by increasing demand for

supporting good and services.

sugar plantation

With the early rise of small factories artisan labor was in decline.

Income for self-employed artisans grew more slowly than others as more

manufacturing was being done outside the home in small factories. In the

period prior to the Civil War organized labor was

essentially nonexistent in America. Unions were considered a form of conspiracy, and

had been illegal under English law for centuries on grounds of conspiracy

and treason, given that the unions were in effect organizations of unpropertied workers who attempted to "conspire" together to their benefit

at the expense of their lords and ultimately the propertied interests of the

king. The attitude toward unions as nefarious conspiracies against the

interests of property holders remained in America, and in American law.

Generally the laws of the United States did not recognize any right to

ownership of property created by laborers prior to the Civil War, as any

laws recognizing a right to property inherent in labor would have called the

system of slavery into question as well. However, a

few states passed some laws that eased the restrictions on unions making the

formation of labor unions legal (within those states), however actions such

as strikes and much in the way of exercise of any real power remained

illegal.

From the founding of the country through to the presidency of FDR in the

1930s, the primary populist interests were those of the small farmers. In

the period prior to the Civil War the major economic conflicts of interests

were not between labor and capital owners (because there were so few free

laborers who had any political rights to begin with) they were between

the farmers, the bankers, and the merchants and manufacturers. This is key to understanding

the development of many of America's economic institutions and laws, as well

as American politics.

American populism is historically rooted in socially conservative farming

culture, defined by small capital ownership and the defense of small capital

owners against larger capital owners, especially against banking.

America's small farmers developed a unique economic and political outlook

that was very different from other economic and political platforms around

the world. This is because American farmers did own their own property,

unlike farmers in virtually all other countries, especially Europe. American

farmers were socially conservative, and held tightly to longstanding

Christian notions about interest and banking, namely that all usury

(interest) was a form of theft and should be illegal.

What existed in America, essentially up until the post World War II era,

was a powerful political block rooted in the farmers that was strongly socially conservative,

anti-Semitic, anti-banking, anti-corporate, anti-free-market, anti-labor,

and strongly reliant on the federal government for support and economic

regulation. These populists viewed the east coast financial centers and

industrialists with tremendous suspicion. They sought government control and

regulation of prices, they were strongly opposed to government subsidies for

corporations, they were opposed to the right of foreigners or corporations

to own land in America, and they sought the nationalization of things like

banks and infrastructure so that the federal government could set prices

below "market value" for things like interest rates and transportation fees.

This brings us to major differences between the development of

industrialized capitalism in America and Europe. Capital ownership was never

widespread in Europe like it was in America. The Europeans all went

essentially from feudal systems of government and property ownership

directly to democratic systems of government and the development of

industrialized economies, without a situation in which virtually all

families owned their own capital. The bulk of the European population went from

being serfs to being wage-laborers, whereas in America what happened is that

there was a period of time where virtually all white families were capital owners. In

Europe capital ownership started out highly concentrated under feudalism and

then became slightly less concentrated under democratic industrialized

capitalism, whereas in America capital ownership started out highly

distributed, and became more concentrated under industrialized capitalism.

The difference in capital distribution between Europe and America prior

to industrialization is key to understanding the differences in the

development of European and American economic systems and political

cultures. Indeed America is unlike any other country on earth in regard to

its transition from an agricultural economy to an industrialized economy

(which is sometimes used as the basis for the idea of "American

Exceptionalism"). America is

essentially the only country on earth that had an egalitarian society with

widespread capital ownership prior to industrialization. Every other

country, from European countries to Japan to China to India to Russia to the

South American countries, already had highly concentrated wealth with all of

the capital concentrated in the hands of a few at the time that they began

developing industrialized economies (the Dutch being somewhat of an

exception to this).

In Russia and China, obviously, industrialization was preceded by

"Communist" revolutions. What the so-called "Communist" regimes did in these

countries was they stripped the feudal property owners of their ownership and

essentially made the state the owner of everything. Various types of

collective farming systems were implemented with major land redistribution

schemes. This had the impact of

reducing economic inequality and creating more equal wealth distribution

than had previously existed in those countries, but the basis for

industrialization was radically different than in America. In these

countries industrialization was a top down process.

In places like Japan industrialization proceeded again via a top down

process, but in the case of Japan the process of industrialization was

administered by the hierarchy of the imperial Japanese state, with the

property rights of the aristocracy largely intact prior to World War II.

Capital ownership in Japan became more widely distributed after World War

II, but still never went through a phase of widespread individual capital

ownership.

In Europe the process of industrialization was not as top down as it was

in Japan, Russia or China, but it was also not as bottom up as it was in

America either. Different countries industrialized at different rates in

Europe. Obviously Britain was the first country to industrialize. Following

the Napoleonic Wars and the series of political changes that took place in

their wake, there was some redistribution of land and wealth that took place

with the rise of democracies across Europe. France, Britain, and the

Dutch industrialized in the 19th century / early 20th century

through a more bottom-up process than, for example, Germany and certainly the

Austro-Hungarians.

Prior to industrialization land was far and away the most important form

of capital, with slaves being the second most important form of "capital" in

the Americas, and indirectly in Europe, where there was little actual

slavery, but where many of the products of slave labor in the Americas were

destined. The radical shift with industrialization was that land ceased to

be the most important type of capital, being replaced by "intellectual

property" (patents, copyrights) and machinery. The whole feudal

hierarchy was built on land ownership rights, so when land ceased to be the

most important form of capital, and new types of capital, which the feudal

lords did not own, came to create more revenue than land, the power of the

feudal system and the old nobility was broken. This is not to say that land

became worthless or that the feudal aristocracies were cast off and became

nothing, they certainly did not, but industrialization provided the avenue

for the development of a new political class which gained its wealth and

power not from inheritance and taxes, but rather from the creation of new

systems of manufacturing and new technologies.

With industrialization in Europe non-propertied peasants became

non-propertied wage-laborers in the mines and factories. Some craftsmen

became capitalists, but most craftsmen struggled to hold on to their

livelihoods as they competed against the output of factories. In England,

where industrialization began, the new capitalists, i.e. factory and mine

owners, originated from a mix of feudal aristocrats, small merchants, and

poor laborers. Aristocrats had obvious advantages in terms of capital

ownership and the ability to back or start new commercial endeavors, however

the aristocracy was more threatened by the rise of industrialization than they

benefited from it. Small merchants, which had made up a small middle-class

in feudal times, were able to use their modest property to build small

factories, and then, in some cases, to expand these small factories into

larger factories and to develop entire supply-chains, acquiring rights to

resources such as coal, water power, cotton plantations, etc. Among the poor

who became capitalists, most of them got their start by making machines and

then developing patents for new machines. The patents then provided them with

enough revenue to become factory owners themselves.

While the living conditions of the poor in industrializing nations

arguably got worse, the increased productivity of industrialization meant

that the percentage of the population that was poor was reduced and the size

of the middle-class grew significantly. Living standards for the growing

middle-class, in America and Europe, grew significantly during the early

stages of the industrial revolution as the increased productive capacity

produced many more goods at lower costs, making much more material wealth

acquirable for average people.

But while industrialization appeared superficially the same in both

America and Europe, there were significant differences beneath the surface.

In Europe the majority of the population prior to industrialization were

unpropertied peasants, and most of the farming was performed on land owned

by feudal lords. The manufacturing that took place in feudal Europe was

dominated by large guilds; the middle-class was small and few people owned

their own capital. Thus, with the rise of industrialization, capitalism, and

democracy, European society was already largely divided into "haves" and

"have-nots", already largely divided into the propertied and the propertyless.

In America, however, virtually every white family owned their own capital

at the onset of industrialization. America was a nation of many small

capital owners, mostly farmers, and America had a system of democracy prior

to industrialization. Thus the political and ideological dynamic was

radically different in American than it was in Europe. In America capital

ownership was associated with economic enfranchisement; ownership of one's

own capital was the means by which most of the citizens ensured that they

kept the fruits of their own labor. In Europe the opposite was the case. In

Europe, and most every other country, capital ownership was the means of

disenfranchisement. Because capital ownership was concentrated in these

places under feudalism, ownership of capital was the means by which the wealthy minority

economically disenfranchised the non-propertied laboring majority. So with

the onset of industrialization in America political power and ideological

persuasion were divided primarily between wealthy large

capital owners and populist small capital owners, slaves and unpropertied

laborers were politically insignificant. In Europe and elsewhere the political power was divided

primarily between the large capital owners and the laborers who did not own

capital at the onset of industrialization, since the "small capital owners"

outside of America were only a minor group representing neither a large

segment of the population nor a large amount of wealth and power. In America

during early industrialization wage-laborers were disproportionately women,

blacks, and "fresh off the boat" immigrants, while almost all native born white men

were capital owners. In Europe wage-laborers and capital

owners were of course more homogenous within a given country, so there were

fewer inherent divisions between wage-laborers and capital owners other than

class. This meant that class interests were in sharp focus in Europe, while

class interests were heavily conflated with racial, ethnic, and gender

issues in America.

With the conclusion of the Civil

War roughly 15% of America's population changed overnight from being a legal

form of capital to being citizens. Virtually all of the freed slaves

immediately became unpropertied laborers, and they and their descendents

would largely remain so for generations. This significantly increased the

number of citizens who were non-capital owning workers, but due to the continued

political repressions of blacks and conflicts between white workers and

black workers, this influx of laborers failed to do much to strengthen the

political power of workers in America. In fact in some ways it made political

opposition to the rights of wage-laborers stronger due to efforts to

continue to restrict the rights of blacks by restricting the rights of wage-laborers, which virtually all blacks were.

The period immediately following the conclusion of the Civil War, from

1870 to 1880, saw the fastest rate of economic growth in American history as

industrialization and banking reforms took hold. From the end of the Civil War through to the 1920s what occurred in

America was a rapid decline of individual capital ownership. This was a de

facto consequence of industrialization, improvements in farming, and the

rise of corporations. As farming became more efficient the prices of

agricultural products dropped, in some cases dropping quite rapidly. From the end of the Civil War through the early part of the 20th century the

United States produced an excess of food due to it's heritage as a farming

nation and due to the still massive amount of land available for people to

acquire cheaply or for free. Farming was still the simplest

and most direct way for someone who didn't own their own capital to start

their own business and establish themselves as a capital owner, which

resulted in an excess of farmers, which resulted in the falling agricultural

prices.

The excess of food, which then became a major export of the United

States, also aided

the process of industrialization. As farming became more efficient, fewer

people were needed to work the farms, resulting in more and more children of

farmers leaving their family farms and going into the cities to look for

work. This produced an ample supply of wage-laborers to satisfy the

demands of growing industry. Since women and children were the least

in demand as workers on farms, a large portion of the growing number of

wage-laborers were women and children, which means that wage-laborers were comprised largely of people who were unable to

vote and had very little political power, these being women, children, and

blacks. While blacks were technically allowed to vote,

Jim Crow laws and

other means of disenfranchisement meant that blacks had limited ballot

access and were very weak politically.

With growing industrialization after the Civil War corporations became

increasingly prominent, contributing significantly to the decline of

individual capital ownership. Corporations are legal entities created by the

government through which multiple individuals can come together to combine

their capital to create a "collective individual". Over time these entities

gained virtually all of the same rights as human citizens, in addition to limited

liability and "eternal life". With the rise of industrial capitalism the

collective power of combined capital led to increases in efficiency against

which individual capital owners could not compete. This led to an increasing

collectivization of capital ownership, largely via the entities of private

corporations in capitalist countries.

The rise of modern corporations was indeed pioneered in America, despite

the fact that many Americans, including some of the nation's founders, were

highly skeptical of corporate power. As noted in a letter to George Morgan

in 1816 discussing the fall of the British aristocracy, Thomas Jefferson saw

in private corporations, which were many times weaker than they are today,

the potential for the creation of a new American feudalism.

It ends, as might have been expected, in the ruin of its people, but

this ruin will fall heaviest, as it ought to fall on that hereditary

aristocracy which has for generations been preparing the catastrophe. I

hope we shall take warning from the example and crush in it’s birth the

aristocracy of our monied corporations which dare already to challenge

our government to a trial of strength and bid defiance to the laws of

our country.

Letter to George Morgan, November 12, 1816

In

Europe corporations had existed for centuries, but their rights and duties

were much more tightly restricted; they were typically only given charters

for a finite period of time, and the issuing of a charter for incorporation

was granted only rarely. Most corporations in the 18th and early 19th

century were not-for-profit, with large numbers of them being educational

institutions, like universities. Corporations were not even allowed in

finance at all under English law, with the sole exception of the Bank of

England, which, while initially privately owned during feudal times (by the

nobility), was also highly regulated and controlled by the government.

In America, however, corporate law was left up to the states, and the

states developed very liberal laws regarding corporations in efforts to

attract capital to them. Indeed the Constitution of the United

States contains no provisions that deal with incorporation, because the

Constitution was written at a time when corporations were not very common

and the overwhelming majority of property was held by individuals, not

collective groups. The entire Constitution deals only with individual

rights, and has no provision for collective rights. In order to address this

problem, corporations came to be defined as individual persons by the mid

19th century. This was done in part because all contract law

was based on relationships between individuals, so in order to meet the

existing precedents of contract law the corporation was defined as a

distinct individual, so that the corporation itself could enter into binding

commercial contracts. What this did, however, was it essentially shielded the

actual individual people who came together to form the corporation from much

legal responsibility, putting the legal responsibilities on the corporate

entity, not real humans.

As of the early 19th century in most states corporations were barred from

making any political contributions, they were barred from owning stock in

other corporations, they were barred from engaging in any activity,

charitable or otherwise, outside of the specific purpose of their charter,

corporate officers were not protected from liability for corporate acts, and

corporations had to be accountable to the state legislators, who had to have

access to their books and could, and did, revoke the articles of

incorporations if a corporation was deemed not to be acting in the public

interest or was exceeding the bounds of its charter. The general legal trend from the mid 19th century through to

the beginning of

the 20th century was to continuously remove these types of restrictions and grant more and more power to corporations. By

the early 20th century corporations, not individuals, had become the

dominant capital owners. The intellectual justification by elected officials

and judges for granting increasingly more power to corporations and in providing

government support to foster their growth, was that these entities, by the

very nature of their size, were more efficient at production than smaller

entities. Large corporations that owned vast amounts of capital were better

able to produce more goods at lower costs, and thus, the argument went,

granting them more power and allowing them to reap massive profits was an

acceptable price to pay for the increased productivity that these

corporations produced. Of course there were other reasons why elected

officials in particular supported the interests of growing corporations,

namely the financial support provided to them by those who sought their

support, and of course ideological sympathy for the growth of powerful

private institutions.

Between the Civil War and the beginning of the 20th century numerous

powerful monopolies emerged and these monopolies were essentially given the

blessing of government, with the belief that the economies of scale created

by these monopolies would yield benefits that would exceed any negative

consequences. There were an astounding number of corporate

mergers around the turn of the 20th century. From 1895 to 1904 over 1,800

manufacturing businesses merged with rivals, with 30% of these resulting in

new corporations that controlled over 70% of market share (today's legal

definition of a monopoly). Even in cases

where mergers didn't take place, collusion was a standard practice of the

day. Because rapid industrialization resulted in business models that

involved high fixed costs and an uncertain market, the intense competition of

the early phases of industrialization made investment in capital highly

risky and often unprofitable. As a result it was common for "competitors" to

collude to fix prices in such as way as to guarantee that all of the

businesses would reap profits. Businesses at this time also colluded against

organized labor and workers in general. They colluded both on the side of

commodity price fixing and on the side of fixing the wages paid to workers

in order to keep wages down.

A significant difference between the development of private enterprise in

America and Europe at this point was that in America there were more laws

against the formation of cartels than in Europe. Because of this, in Europe

businesses tended to remain smaller and independently owned, but to form

cooperative cartels in order to reap the benefits of larger organizations.

In America however, since cartel agreements were largely illegal in private

industry, this led to more mergers and consolidations, where companies

simply merged to form larger organizations. The net result was more rapid

consolidation of capital ownership in America than in Europe.

By the 1870s there were growing political pressures to regulate large

corporations, particularly the railroads. By this time the railroad

companies were the largest companies in the country, and they were rife with

corruption and price fixing. The railroads were all technically private

enterprises, but they had been granted many public advantages, such as land

grants, rights of eminent domain, and many government

subsidies. Complaints against the railroads for price fixing, both by

passengers and shippers, were the most common, but the most effective

political and legal pressure against the railroads came from the farmers,

who had become dependent upon the railroads to ship their harvests to

market. Yet at this time very little was done in the way of federal

regulation of private enterprise. While the federal government did plenty to

subsidize and assist the development of private enterprise, little was done

to regulate it.

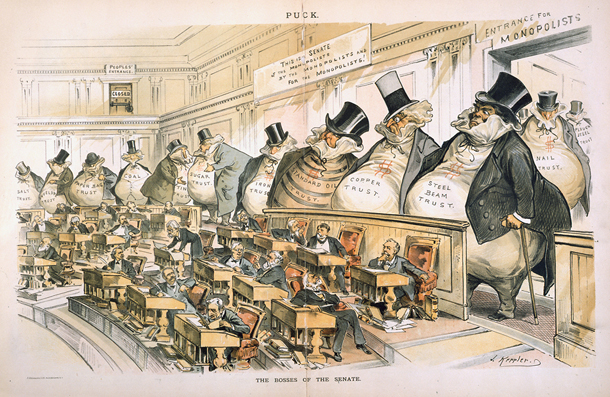

By the1890s there was widespread public outrage at the actions of "big

business" and widespread fear of the growing power of large corporations to

manipulate prices and to drive down wages, in addition to the growing

understanding that corporate money ruled Washington, yet little was

being done to address these concerns at the federal level.

The Bosses of the Senate 1889

In 1890 the

Sherman Antitrust Act was passed. The Sherman Antitrust Act is still one

of the most significant federal laws affecting businesses today, as it is

effectively an anti-monopoly law. The law basically prohibits a corporation

or corporations from engaging in behavior that significantly reduces

marketplace competition. In other words, this law requires that competition

exist with the exception of so-called "natural monopolies". Ironically,

however, this law was first applied against unions to bust strikes, under

the reasoning that the unions were operating a conspiracy to form a labor

monopoly, thereby reducing "competition" in the labor market. Despite the

passage of the Sherman Act, little was done to regulate private enterprise

or to enforce the Sherman Act against corporations.

This all changed with the presidency of

Theodore Roosevelt from 1901-1908, who took significant action to

regulate "big business" at the federal level. The "trust busting" activates

of Roosevelt consisted largely of breaking up large national corporations

into smaller independently owned companies and forcing them to compete

against one another. Roosevelt also presided over increased regulation of

interstate commerce, especially in regard to the railroads.

What had happened in America from the end of the Civil War up to

Roosevelt's presidency was that corporations and private enterprise had

grown well beyond their original local scope. Prior to the Civil War there

were practically no interstate businesses. There was interstate commerce,

but it was almost entirely commerce between separate local businesses. After

the Civil War, with the establishment of a

National Banking System, the rise of industrialization, and the

development of rail roads, there was

an explosion of companies that operated across multiple states, with workers

and capital and owners residing all across the country. In addition, the

prior conditions which naturally led to markets populated by many small

independent actors had given way to markets dominated by monopolies or small

numbers of large corporations. The idea that business was not originally

heavily regulated in America is a misnomer, there have always been

significant business regulations in America and things like price controls,

and the establishment of government backed monopoly enterprises for the

public good, such as public utilities, etc. were in place from the founding

of the country. The difference is that prior to the 20th century all of the

regulation took place at the state level. Since virtually all businesses

existed only at the state level prior to industrialization, and since

businesses were naturally small and less powerful than the state

governments, this wasn't a problem. When businesses expanded rapidly in size

after the Civil War and quickly became more powerful than not just state

governments, but in many ways more powerful even than the federal government

as well, this is what prompted the widespread support for federal regulation

of private enterprise.

The

economic panic of 1907 demonstrated multiple fundamental problems with

the American economy and paved the way for significant changes, including the

creation of the Federal Reserve. The panic of 1907 was brought about by

massive bank failures resulting from massively over-leveraged stock-market

trading schemes in the largely unregulated New York Stock Exchange. Traders

were borrowing astronomical sums of money in attempts to corner the market

on stocks and drive their prices. In one such case the attempt of one

borrower failed resulting in massive losses by the trader. Those losses were

all on borrowed money, and the amount of money that was borrowed was so huge

that the multiple banks which had lent the money immediately failed due to

runs on the banks.

The stock market quickly lost 50% of its value and runs on the banks

around the country led to multiple bank failures virtually overnight. This

demonstrated a clear need for greater regulation of the stock exchanges and

lending practices, as well as weaknesses with the banking system, but

additional events would demonstrate not only the weakness of the

government's ability to address these problems, but also the ways in which

America's wealthy industrialists had become more powerful than the

government.

As the crisis deepened, the government was effectively impotent to do

anything about it. J.P. Morgan and John Rockefeller stepped in to address

the problems by overseeing the liquidation of various banks, buying

companies, and depositing reserves in remaining banks (as loans). Morgan and

Rockefeller contacted other wealthy Americans and acquired pledges of

massive loans to keep the American banking system propped up. While there

was relief that these individuals did step in to avert greater crisis, it

also demonstrated how weak the government was and how disorganized and

unready the nation was to handle the realities of the modern economy.

Despite the reforms of the early Progressive era at the beginning of the

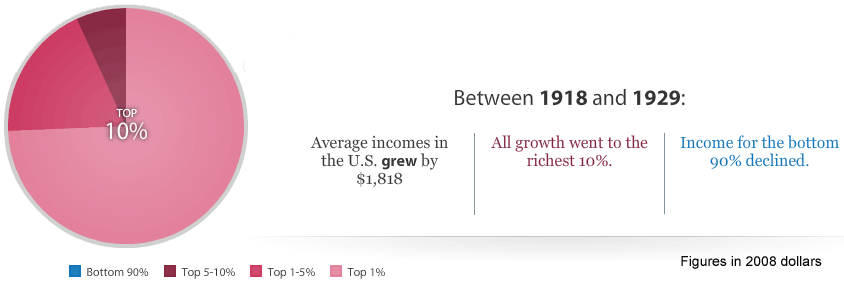

20th century, the general economic trend remained the same. While large

national corporations had been broken up into smaller companies and forced

to compete against each other, the trend was still toward larger aggregation

of capital and higher concentration of capital ownership. The percentage of

farmers and the self-employed continued to decline and the portion of the

population who were wage-laborers increased as continued industrialization

increased efficiency and made smaller business operations unable to compete

with larger national or regional corporations.

After Teddy Roosevelt's reforms, and laws passed to strengthen the

role of unions, there was a brief period prior to the end of World War I in 1918

when union membership increased and wages and working conditions

improved. During this time economic inequality was on the decline,

however after the 1917 Communist Revolution in Russia, and the

conclusion of the Great War, the tide turned against organized labor, and

along with decreasing industrial demand due to the conclusion of the war

in addition to the return of men from over seas, labor's share of the

national income began declining and economic inequality began to rise

again. By the 1920s the old American economy grounded in farming and

widespread individual capital ownership was essentially gone, with

production now dominated by corporations employing wage-laborers.

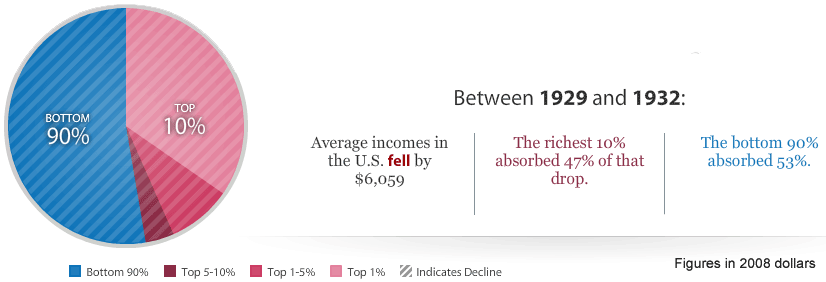

Prior to World War I the United States was a debtor nation, with the

country being in almost continuous public and private debt to foreign

countries since the day of its founding. However World War I changed this.

All of America's foreign debts were eliminated via America's contributions

to World War I and post-war pledges of reconstruction aid to Europe. This

elimination of the debt via the war paved the way for a massive explosion of

household and business credit in America, which helped to fuel the economic

excesses of the 1920s and played a significant role in creating the economic

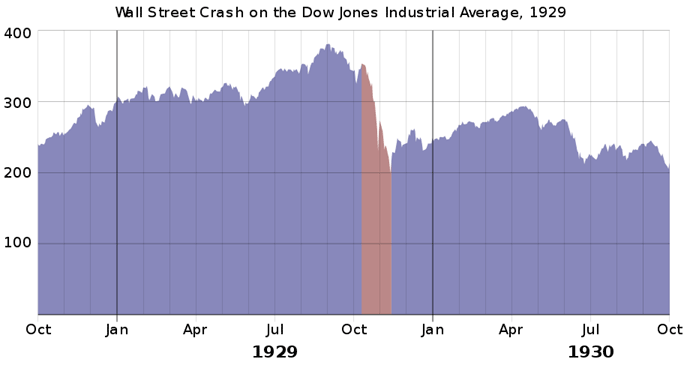

bubble that burst in 1929, followed by the Great Depression.

The 1920s was the first time in American history that most major

purchases were made using credit. During this time 75% of cars were

purchased on credit, 70% of furniture, 75% of radios, and 80% of household

appliances were all purchased on credit. This explosion of credit enabled an

explosion of productive capacity, which allowed prices to stay fairly stable

in the face of major expansions of the money supply, both in terms of

real money supply created by the new Federal Reserve, and the virtual money

supply created by all of the credit. Even though one might expect rising

inflation, in fact inflation stayed under control due to rapidly expanding

productive capacity, as industrialization blazed ahead at break-neck speed.

During the 1920s wages did continue to rise modestly in real terms overall, but with the

decline of organized labor a larger and larger portion of the value created

by corporations went to capital owners and executives instead of the workers. Industrialization was increasing efficiency so fast that the real

economic gains were able to be shared by virtually everyone (who was white),

though this was largely due to credit.

The real gains in productivity, the massive expansions of credit, in

addition to the fact that a disproportionate share of the gains were going

to capital owners, all contributed to the rapid rise of stock prices. The

rapid rise of stock prices during the 1920s was largely a product of two

things, the growing savings of the wealthy who were looking for something to

do with their money to get a return on investment, and credit financed

speculation. As was

the case leading up to prior American stock market crashes, stocks were

highly leveraged with major amounts of credit. Low interest rates and

rapidly rising stock prices induced speculators to buy on credit amidst a

widespread faith that prices would rise indefinitely, with stock brokers and

lenders happy to facilitate the transactions for the short-term fees they

generated. In 1900 roughly 1% of the American population owned stocks, and

by 1929 over 10% of the population owned stock. Because of the fact that the

unemployment rate remained very low, prices

were stable, and wages were rising, the overwhelming majority of economists

believed that America had entered a "new era" of economics, where government

intervention had become unnecessary and prices, productivity, and profits

would rise forever.

The overwhelming majority of economists and public figures were touting

the fundamental strength and soundness of the economy right up until the

crash in late 1929, however this view was not universal. There were

economists and scholars who did warn of an impending crash. In February of

1929 the newly created Federal Reserve, feeling that credit based speculation

had gotten out of control, announced that it would no longer support bank

loans for stock purchases. Famously, Roger Babson warned that, "Sooner

or later a crash is coming, and it may be terrific ... factories will shut

down ... men will be thrown out of work ... the vicious circle will get in

full swing."

While most people focus on the stock market crash, the stock market crash

did not cause the ensuing Great Depression, the crash was a symptom of the

fundamental underlying economic problems, and the true depression did not

take hold for over a year after the crash.

The

reason for the overall economic crash, though much debated, was largely over-borrowing by

consumers, who were unable to ultimately pay back their loans resulting in spending

being unable to keep pace with productivity as the share of income going to

workers declined. Thus, productive capacity had expanded at a higher rate

than consumptive capacity. The massive expansion of credit served as a means

to bridge the gap between productive capacity and consumptive capacity, but

ultimately, since wage growth never caught up to productivity growth, the

credit bubble burst and demand rapidly plummeted. By 1929, both the consumer

markets and the stock market were highly leveraged on credit. By mid 1929

retail sales were in decline and by September stock prices had begun to

fall. In October of 1929 rapid decline of stock prices was underway.

The crash of the stock market in 1929 didn't directly cause unemployment

or factories to close. Again, the crash was a symptom not a cause. The cause

was fundamental lack of aggregate demand. The economic crash started in

America and quickly spread around the world. At the time of the economic

downturn America was the largest consumer market in the world. Europe was

still recovering from World War I, and no other countries were yet

sufficiently industrialized or had sizable middle-classes. When demand

collapsed in America due to the working-class not having enough income or

wealth to consume the goods that were being produced, there were no other

global consumers to step in to prop-up demand either, and thus sales rapidly

declined, resulting in the closing of factories, resulting in growing

unemployment, resulting in ever shrinking demand, resulting in more

factories shutting down, resulting in retail stores shutting down, resulting

in growing unemployment, resulting in people losing their homes, resulting

in more loan defaults, resulting in shrinking demand, resulting in factories

shutting down, resulting in growing unemployment, etc., etc., etc.

In the months and years following the crash of 1929 most people expected

that the economy would improve and the stock market would gradually return

to its peak levels. This was not to be. The unemployment rate went from 3.2%

in 1929 to a high of 24.9% in 1933 when Franklin D. Roosevelt entered the

presidency.

The details of the Great Depression and the New Deal are complex and much

debated. From a high level, however, what must be said is that FDR entered

office in 1933 and died in office in 1945, a span of 12 years, and during that

time Roosevelt maintained strong public support and unprecedented

legislative power, which was used by the Roosevelt administration to

significantly change the structure of the US economy and the role of the

federal government in the regulation of the economy. In the short term, the

most significant actions taken by the Roosevelt administration were the

regulation of banks, requiring citizens to return all gold coins and gold

certificates to the US Treasury, destruction of agricultural stocks in order

to raise prices, and the creation of public works programs

to provide jobs for the unemployed.

Over the long term the major impacts of the Roosevelt administration were

increased regulation of the economy by the federal government, the creation

of major social safety net programs, expansion of the federal tax base, and

the adoption of a highly progressive income tax system. What the Roosevelt

administration did not do was it did not fundamentally change the structure

of the capitalist economy. The effect of the New Deal was to regulate

capitalism, not to change its fundamental structure. FDR's policies were

seen at the time, and in retrospect, as a means of mitigating the excesses

of capitalism, while allowing the fundamentals of the system to remain

unchanged. The stock market remained in place, the relationship between

capital owners and wage-laborers remained in place, the rights of property

ownership remained in place, system of private banking remained in place,

industries were not nationalized, boards of directors stayed in place at

corporations, profit motive remained the prime driver of business,

etc. yet restrictions were placed on all of these things. Banks remained

private, but they had more rules they were required to follow. Profits from

capital gains remained in place, but they were more heavily taxed. Wages

remained largely determined by individuals within a labor market framework,

but minimum wages were implemented and collective bargaining was officially

sanctioned by the government.

It is important to note that the changes brought about by the Roosevelt

administration were broadly supported by the American public. Indeed FDR was

one of the most popular presidents of all time during his own presidency. At

the time that FDR was in office the Democratic Party, of which he was a

member, was still largely a Southern party, and it was a party heavily tied

to farmers. The political support of American farmers and Southern social

conservatives was essential in the passing of Roosevelt's New Deal agenda. Indeed this is

why many of the benefits of the Roosevelt administration's programs went to

rural Americans. Rural Americans received a disproportionate amount of the

benefits of the public works and economic development programs of the

New Deal era. Rural electrification, road building, dam

building, farm subsidies, etc. all primarily benefited rural Americans and

family farmers who, at this point in American history, while dwindling as a

percentage of the population, still represented about 25% of the American

population and were powerful politically. In 1933 only 10% of American farms

had electric service and by 1940 over 90% did, nearly all of it provided by

federal government programs.

The Roosevelt administration did make attempts at planned economy,

through various government direct-employment programs, production targets

for industries, financial incentives for targeted industries, etc., but the

problem with much of this is that while much of the fundamental planning may

have been sound, by the time these plans were implemented they had been so

distorted by political wrangling and horse-trading that priorities

were often set more by the political bargaining of special interests than by

sound economic policy.

During the 1930s there was a high degree of corporate consolidation.

Business leaders and many economists placed the blame for the depression on

excess competition, and thus sought to reduce restrictions on collusion and

anti-competitive practices. The Roosevelt administration basically went

along with this

assessment and created agencies to regulate and oversee the consolidation of

businesses and to allow greater collective bargaining among businesses, in

other words to allow forms of collusion. The result was that, both due to

the natural tendency of consolidation after an economic crash, and due to

government policies that facilitated consolidation, capital ownership

actually became much more highly concentrated during the 1930s than it was

previously.

The net effect of the Great Depression on capital ownership was that the

percentage of the population who owned stocks was dramatically reduced from

the height of 1929, the corporations that did survive the crash generally

got bigger as competitors went out of business or were consumed by mergers,

investments in capital declined significantly, startup businesses declined,

and patent applications declined, but not dramatically. The percentage of

the population working for themselves did increase, but this was out of

desperation not opportunity, and few of these self-employed people managed

to amass any capital or develop meaningful businesses. Many of those who

were "self-employed" out of desperation engaged in services or were small

time merchants, with their primary asset remaining their manual labor.

Overall, during the 1930s (and several decades beyond) both the size of

corporations and government grew. Both government and large corporations

accounted for an increasing share of employment over this period.

source: Historical Statistics, series D86; Michael Darby, Journal of

Political Economy, Feb 1976, p. 8

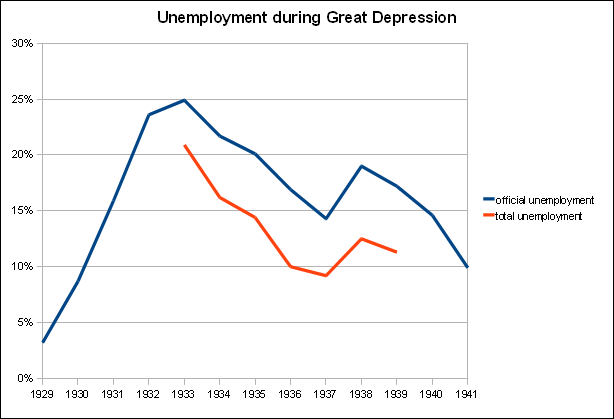

The various public works programs implemented by the Roosevelt

administration were programs for the unemployed, and as such, workers in

those programs were still considered to be unemployed. Roughly 5% of the

workforce was employed through public works programs throughout the duration

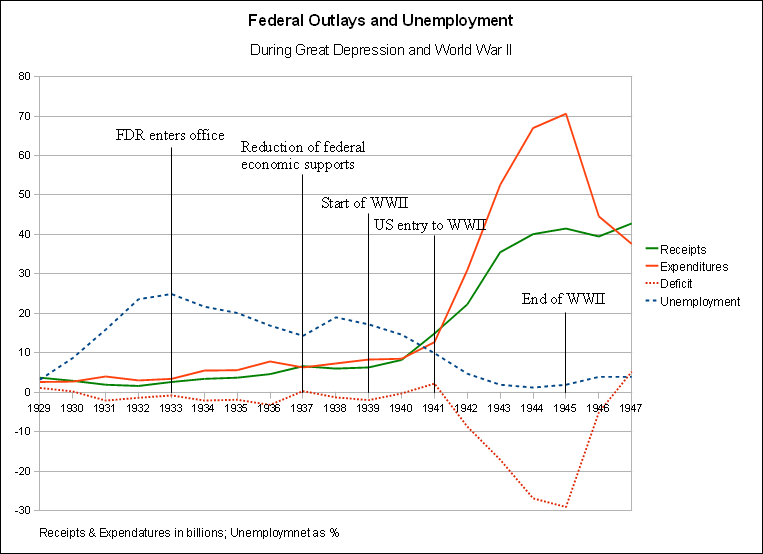

of their implementation. The graph above shows the official unemployment

rate in blue and the total unemployment rate when counting all those

employed through the public works programs for the unemployed as employed.

The official unemployment rate did decline from 1933 to 1937, but rose

again in 1938 after the Roosevelt administration, facing pressure from

opponents and worried about the national debt, started cutting back on

direct aid to the economy. By 1940 American production related to World War

II had already begun, even though the US would not officially enter the war

until December, 1941 after the attack on Pearl Harbor.

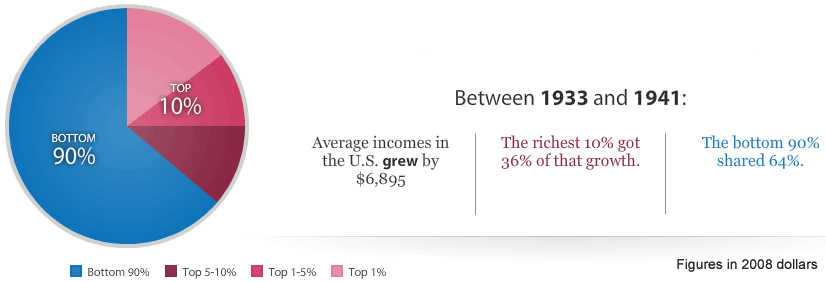

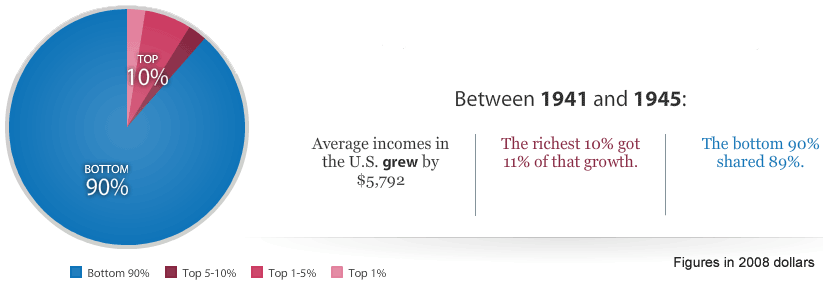

Income inequality fell only slightly during the 1930s and was not

significantly reduced until after World War II. One of the reasons that

unemployment remained high throughout the 1930s was that, despite

significant government expenditures and works programs, consumer demand

remained very low. Among those who were employed, the threat of losing one's

job led them to put most of their excess income into savings, to save against

the prospect of joblessness. Even though significant money was being saved,

people greatly distrusted banks so relatively little of the money was saved

in private banks, where it could have been lent out. Likewise, private banks

had become highly risk averse and since interest rates were so low, they had

little incentive to lend. The result was increased savings, but no

corresponding increases in lending or investing. Consumer demand remained low,

so there was

still nothing to significantly drive production, thus there remained little

reason to hire workers since excess productive capacity remained in the

system.

America's entry into World War II changed all of this by creating an external

driver of significant demand. The American wartime economy of World War II

can in some sense be thought of as the New Deal on steroids. The structuring

of the government's role in the economy during the 1930s provided a strong

framework through which the federal government was able to effectively take

control of the American economy during World War II and command production

through a centralized system. The wartime economy of the US during World War

II is the closest that the country has ever come to a fully centrally planned

economy.

During Word War II the Roosevelt administration created the National

Defense Advisory Commission (NDAC),

Nation Defense Research Council (NDRC),

War Production Board (WPB),

Office of Price Administration (OPA), and

Office of War Mobilization (OWM). Many of the agencies created under the

New Deal to deal with the economy were eliminated during World War II and

supplanted by these new wartime production agencies. Through these and other

agencies the federal government gained almost complete command over

the entire economy. Virtually all prices were fixed or had caps set on them.

These pricing caps were set out in huge manuals that were delivered to

businesses, covering everything from steel to mayonnaise. Practically

every material was rationed. Production and raw material extraction

facilities were either built directly by the government when needed, or the

government paid private companies to expand or modify their existing

facilities for wartime production.

source: US Bureau of Economic Analysis, National Income and Production

Accounts, Table 1.1 & Table 3.2

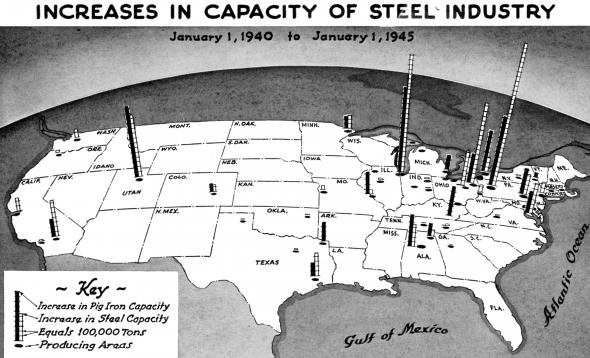

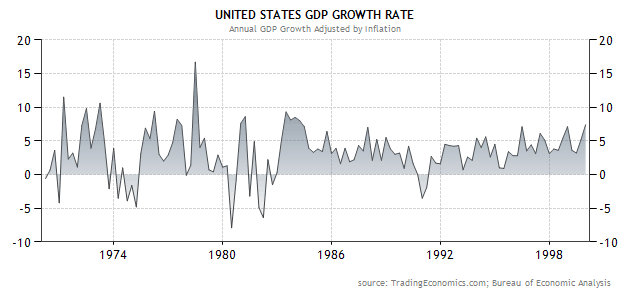

From 1939 to 1944 GDP practically tripled and unemployment was cut from

roughly 18% down to around 1% entirely through the massive

infusion of government spending and economic controls. What the war had

done, essentially, was provide the political will to fully engage in a

Keynesian government-directed economic stimulus program. While the New Deal

programs of the 1930s seemed large at the time, they were smaller than what

was being recommended and sought after by Roosevelt. While there was

widespread popular support for the New Deal stimulus programs, there had

also been strong and focused opposition largely from wealthy private

citizens and from politicians and economists both for ideological reasons

and out of a genuine belief that government spending and government programs

would undermine the economy and prevent a recovery. There was serious

concern during the 1930s about the federal deficit and the debt being

accumulated by the government, and this made it difficult for the Roosevelt

administration to engage in truly significant economic stimulus. What the

war economy showed, however, was that, given enough control and enough

spending, the government was capable of significantly stimulating the

economy and creating full employment, at least in the short term.

After World War II many economists wondered if the Great Depression could

have been ended much sooner had World War II level stimulus been applied in

the early 1930s. This is a difficult question. Theoretically it would seem

that the answer is yes, but it isn't quite that simple. It is not clear that

it would have been possible to engage in the level of borrowing and deficit

spending that was exercised during World War II during the 1930s, and that

even if the money could have been borrowed it may not have been as easy to

repay as it was after World War II. During the war the Europeans were

obviously willing to lend virtually unlimited sums to America. In addition,

the war made it politically possible to raise taxes to a degree that hadn't

been possible prior to the war. Taxation came to be seen as a patriotic duty

for national self defense during the war, and it was during World War II

that the tax base was significantly expanded and tax rates were

significantly increased. A significant amount of money was also raised from

war bonds, purchased by American citizens, and people just wouldn't have

bought bonds in that way for any reason other than war. Likewise, after the

war it was easier for America to pay down the national debt because of

agreements made during the conclusion of the war. Importantly, the war left

America as the sole economic super-power in the world, a position it did not

hold prior to the war, which made it much easier to repay the remaining

debts.

So what we can say is that the degree of amassing and paying down of the debt that

fueled the war time economy would not likely have been possible without the

conditions of war. If, in theory, the political will existed in 1933 to

engage in the same type of massive government effort that fueled the war

time economy, and if the same tax increases had been put in

place in 1933 that were in place in the 1940s, it is still not likely that

the government would have even been able to borrow as much money as it did

during the war because lenders wouldn't have been willing to lend it and

citizens wouldn't have bought the bonds, and even if the money could have

been borrowed, paying it back at that time would likely have been much more

difficult than it was after the war. Nevertheless, the experience of the war

economy does indicate that had significantly more government stimulus been

applied during the 1930s, based on increased taxation and deficit spending,

unemployment could have been reduced much more significantly and rapidly.

There was a very important difference between the 1930s and the war

economy of the early 1940s however, and that was the relationship between

government and the private sector. During the 1930s, while there was

certainly cooperation with the private sector and attempts to aid even

the captains of industry, by and large the relationship between government

and the private sector was antagonistic. Roosevelt portrayed corporations

and wealthy bankers and industrialists as the enemy of the people, and

economic policy of the time sought largely to regulate business, not

facilitate it.

When the war mobilization efforts ramped up, however, the opposite became

the case. Roosevelt knew that the nation needed the manufacturing capacity

and know-how that rested almost entirely in private hands in order to be

able to meet the production needs of the war. As such, captains of industry

were invited into the government and took key departmental and advisory

positions. While the government had already been contracting heavily with